The Art and Special Collection Lifecycle

Art and collectibles may comprise a special part of an artist’s, collector’s, individual’s or family’s assets. You want to ensure that your fine art, antiques and other collectibles are protected – now and in the future – and that the people and institutions intended to continue your legacy can and will. (See The Rosalie Thorne McKenna Foundation Case Study: Going the Extra Mile to Fulfill the Artist's Dreams)

While artists, collectors and families have different issues and motivations, and the complexity of their holdings may vary, the basic premise is the same – planning is critical to ensure that you achieve your vision and goals and protect loved ones from unexpected outcomes.

Complex Issues

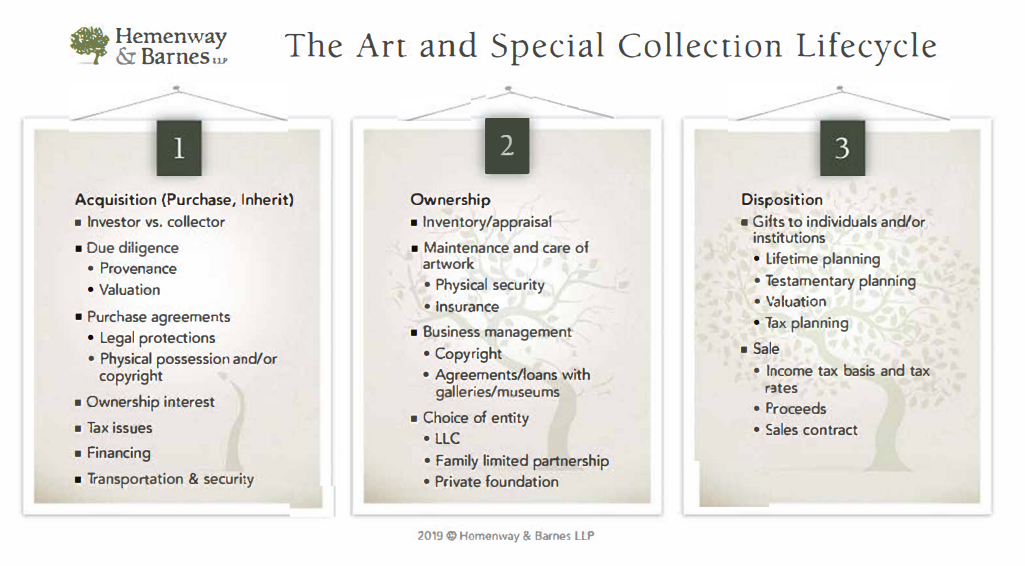

The Art and Special Collection Lifecycle is a useful framework for understanding the various components of the planning process. As with the family home or business, planning for fine art and other collections raises questions, such as:

- Do I know what I have and do I have a realistic estimate of the value?

- Is my art well-maintained and properly insured?

- Can my family afford to keep my collection after I am gone?

- What should be donated, sold or bequeathed?

- How do I fairly divide and distribute my collection among my family and other beneficiaries?

- How can I ensure that my wishes regarding my collection will be honored?

Why Hemenway & Barnes?

Hemenway & Barnes professionals have helped generations of families, collectors and artists manage and plan for their art and other collections. We can guide you through the planning process by helping you:

- Create a plan for your collection that is consistent with your goals and values

- Inventory your collection and work with a qualified appraiser to determine its value

- Assemble provenance documentation

- Develop a tax-wise plan for transferring your art to family or charity

- Minimize estate tax and reduce audit risk

- Resolve copyright and licensing issues

Hemenway & Barnes attorneys and professionals work as part of a full-service team. This affords clients access to the firm’s art-specific experience combined with the expertise of our other practice disciplines. These include tax, trust and estate planning and administration; probate; philanthropic advising; dispute resolution and litigation and real estate.

Clients

Our clients include collectors, individuals, families, artists, foundations, museums and other nonprofit organizations. They seek our counsel for sophisticated art transactions, tax and estate planning and complex regulatory matters.

Representative Experience

Artists

- Design and implement numerous estate plans, including for those with extensive collections worth millions of dollars

- Facilitate charitable gifts of art to museums, archives and other nonprofit organizations

Families

- Design and implement estate plans for individuals and families with art collections or single works, or, other collectibles, including sales and gifting

- Act as a liaison with appraisers, auction houses, fine art transporters and insurers

- Help clients authenticate and establish provenance for their paintings

- Coordinate the sale of family art collections

Charitable organizations

- Establish and manage private foundations to perpetuate an artist’s or collector’s legacy and to manage the artwork

The Rosalie Thorne McKenna Foundation Case Study

In the course of her long career, Rollie McKenna created an archive large enough to fill three rooms. Despite her inherited wealth and stated wish to establish a foundation to preserve her art and provide opportunities for young photographers, her estate plan proved inadequate to carry out her wishes. Two years after her death, her legacy remained neglected and uncataloged in a warehouse outside of Boston.