New Proposed Donor-Advised Fund Regulations May Broaden DAF Treatment, Chill Donor Involvement, and Threaten Tax Deductions

On Tuesday, November 14, 2023, the Treasury Department issued new Proposed Regulations for donor-advised funds (DAFs) which will dramatically affect many charitable funds. In particular, these Proposed Regulations, if made final, will subject many funds that are not currently treated as DAFs to the restrictive DAF rules, will significantly curtail certain common DAF structures and strategies, and may threaten tax deductions for contributions to a broad array of charitable funds where donors may serve on committees or in other advisory roles.

The Pension Protection Act of 2006 imposed extra rules on DAFs that do not apply to non-DAF funds at public charities. Those rules include:

- Restrictions on distributions: Section 4966 of the Code taxes DAF sponsoring organizations on distributions from DAFs to any organization other than certain public charities without satisfying the “expenditure responsibility” requirements, distributions to individuals, and distributions for non-charitable purposes.

- Restrictions on benefits to donors or advisors: Section 4967 of the Code taxes donors, donor-advisors, and potentially fund managers whenever a donor or donor-advisor receives any more than incidental benefit as a result of a DAF distribution.

- Preclusion of grants, loans, compensation or similar payments to donors or donor-advisors: Section 4958(c)(2) of the Code treats any grant, loan, compensation or similar payment to a donor or donor-advisor as a per se “excess benefit” transaction, subject to tax.

- Extra substantiation requirements: Section 170(f)(18) provides that donors to DAFs will not receive any tax deduction if their acknowledgement letters do not (in addition to the requirements for standard acknowledgement letters) include an extra disclaimer that the DAF sponsor has exclusive legal control over donated assets.

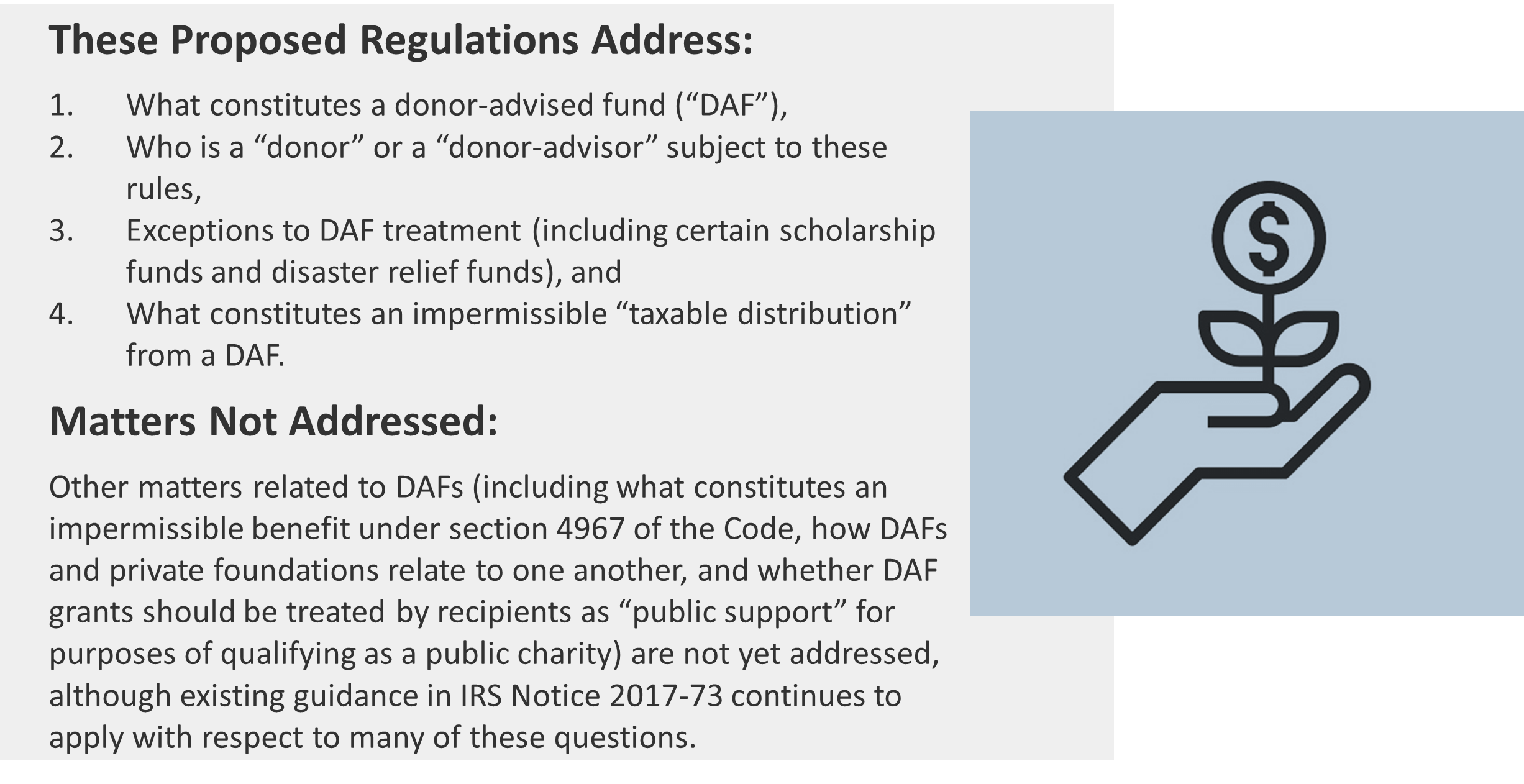

Continue reading for highlights from the Proposed Regulations that might affect current DAF holders and structures including:

- Ability to Use Compensated Personal Investment Advisors for DAFs Effectively Precluded

- Definitions of Donor-Advised Fund, Donor, and Donor-Advisor

- Taxable Distribution Rules

- Potential Threat to Income Tax Deductions

- Applicability

Brad Bedingfield

Brad assists private foundations and public charities with navigating complex tax regulations and procedures, including receipt and disposition of complex charitable gifts and participation in innovative forms of impactful philanthropy.