2024 Personal Tax Planning Update

The new year brings with it new tax-savings opportunities, including opportunities for tax-free gifts. The charts below show the larger gift and estate tax figures, as well as this year’s federal income tax brackets. Now is the time to consider federal estate and gift tax strategies before exemptions are scheduled to decrease by 50% in 2026.

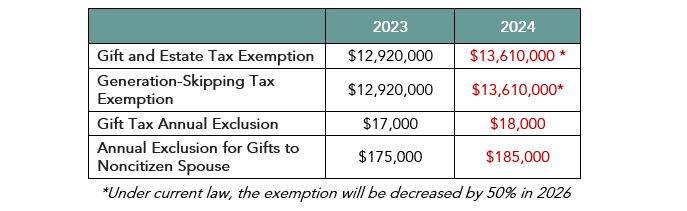

Federal Estate and Gift Tax Exemption/Exclusion Levels

Below is a chart showing the gift and estate tax figures for 2024, reflecting the annual inflation adjustments from the Internal Revenue Service.

The larger gift and estate tax exemptions and exclusions mean additional opportunities for tax-free gifts in 2024.

- Make Annual Family Gifts Early – The “annual exclusion” now allows you to transfer up to $18,000 ($36,000 for married couples) to any individual. Making these gifts early in the year often results in more value passing to family members at no additional tax cost because it allows any appreciation over the year to pass to the recipients free of estate or gift tax.

- Make Use of the Larger Transfer Tax Exemption, Including Inflation Adjustment – With higher inflation rates, there was a significant bump to the annual inflation-adjusted estate/gift tax exemption and the generation-skipping transfer (GST) tax exemption. These exemptions increased to $13,610,000 in 2024 (up from $12,920,000 in 2023). Married couples are now able to give away $27,220,000 without gift or GST consequences. Even individuals and couples who have already used their entire prior exemptions now have an additional $690,000 (or $1,380,000 for married couples) that can be gifted in 2024. Making these gifts early in the year will ensure that they are accomplished and allow any appreciation in the assets to pass to the recipients free of estate or gift tax. Beginning in 2026, these exemptions are scheduled to be cut in half (approximately) from their current levels. Anyone in a position to take advantage of these larger exemptions who does not act prior to 2026 risks missing a potential opportunity to save millions in taxes. While it is possible that the larger exemptions could be made permanent, it is also possible that the exemptions will be reduced prior to the 2026 sunset date. The IRS has indicated that it will not seek to “claw back” any use of this additional exemption once it reverts to its old level.

- Large Gifts to Spousal Lifetime Access Trusts – One strategy for using the larger exemption for married couples is a specialized type of trust, called a spousal lifetime access trust (often abbreviated “SLAT”). SLATs include one of the spouses as a beneficiary, thereby preserving the possibility for a spouse to receive distributions from the trust if needed. This safety net often makes donors more comfortable with making large gifts, allowing them to take advantage of the current high exemptions.

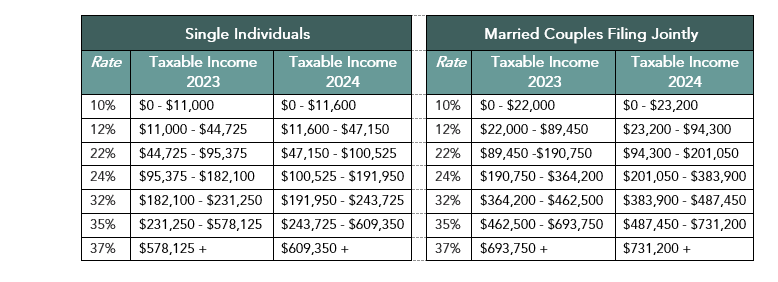

Federal Income Tax Brackets for 2024

Federal income tax rates have not changed for 2024, but the break points of the various brackets have been adjusted as shown in the charts below. (Note that lower rates continue to apply to income from qualified dividends and capital gains.)

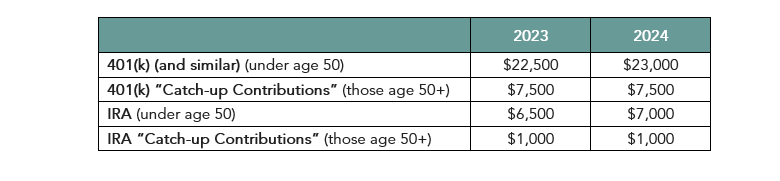

Retirement Account Planning

The SECURE Act of 2022 (SECURE 2.0) raised the age at which required minimum distributions (RMDs) must be taken. As of January 1, 2023, RMDs must begin at age 73 (up from age 72). The additional year can allow extra tax-free growth of assets in retirement accounts. For more details on the changes under SECURE 2.0, see Important Retirement Account Changes Under the SECURE 2.0 Act of 2022.

The maximum contributions for retirement accounts have also increased for 2024 (for the most part). Consider adjusting your pay-ins accordingly in order to maximize these tax-efficient savings.

Charitable Planning with Retirement Accounts

For close to two decades, retirement plan owners who are at least age 70 ½ have had the ability to give up to $100,000 per year to charities directly from their IRAs as qualified charitable distributions (QCDs). Such QCDs would count towards a plan owner’s RMD and not be included in the plan owner’s taxable income. The QCD is adjusted for inflation, and the 2024 limit is $105,000. SECURE 2.0 added an additional benefit—it also permits a QCD of up to $53,000 per lifetime (not annually) to certain “life income” charitable vehicles, such as charitable gift annuities, charitable remainder unitrusts and charitable remainder annuity trusts.

For more details on the expanded opportunities for charitable giving with retirement assets, see Expanded Opportunities for Charitable Giving with Retirement Assets.

529 Plan Rollover to a Roth IRA

Another provision of SECURE 2.0 that goes into effect in 2024 allows 529 plan beneficiaries to roll over unused funds to a Roth IRA owned by them. Individuals who have owned (or been a beneficiary of) their 529 for at least 15 years are allowed to roll over up to $7,000 per year (or more, based on the annual IRA contribution limits) to their Roth IRA, with a total lifetime rollover limit of $35,000. This could be a good option for those who have funds remaining in their 529 plans after they have completed their education.